Hong Kong’s Budget Deficit: Causes and Cures for a Sustainable Fiscal Future

Tim He

Hong Kong must prioritize long-term revenue diversification over short-term cost-cutting.

Over the past few days, the Department of Finance and Financial Secretary Paul Chan have likely been working

intensively to identify feasible government spending cuts in order to achieve a balanced budget, as mandated by

Article 107 of Hong Kong’s basic law. The government’s largest areas of expenditure have come under scrutiny, with a

variety of spending cut proposals such as the adjustment of the $2 public transport scheme, the freezing of civil

servant salary, and even raising fees for non-urgent accident and emergency public hospital room visits. Although

these cost-cutting measures may provide some relief in the short term, it does not address the crucial issue of the

government’s over reliance on land sales and taxes for revenue generation.

Government land premium revenue, constituting around 20% of total government revenue post-Covid, dropped to $3.7b

as of October 2024, missing the government target of $33b by 88.8% and marking a decrease of 81% from the 23/24

fiscal year. Other non tax revenue such as investment returns, which makes up 13.9% of total revenue in 23/24, are

highly volatile and subject to unpredictable market fluctuations. Simultaneously, Hong Kong faces a rapidly aging

population which necessitates increased government spending on areas such as transportation and healthcare. This

demonstrates how over reliance on relatively undiversified income sources can increase vulnerability in government

finances. Thus, to balance the budget in the long run, we should aim to explore a range of options for further

revenue growth instead of cutting expenditure revolving around critical public services such as transport,

education, and healthcare.

Initiatives by the government for long term economic growth such as the Lantau Tomorrow Vision and the Northern

Metropolis could help reach this goal. However, some of these infrastructure projects unfortunately face delays

amidst the current financial turmoil, alongside negative public sentiment. Further private sector involvement in

partially shouldering the financial burden of such projects should be pursued to reduce current government

expenditure but still continue their development.

In conclusion, it is not to say some short term adjustments are not necessary or helpful, or that we have not

looked into any plausible alternatives, but more attention and emphasis should be given towards possibilities

surrounding sustainable revenue generation and growth.

Economic History: Parallels between Trump’s “Liberation Day” and Hoover’s Smoot-Hawley

Sebastian Zhu

Donald Trump, the 45th and now 47th US president, announced on the second day of April a series of “reciprocal

tariffs” on countries from China to the Falkland Islands, a remote archipelago known for penguins. The quantity of

tariffs is unrivaled in recent history: tensions quickly escalated, sparking an international trade war with

retaliatory actions taken by China and the EU.

“We should beware of the demagogues who are willing to declare a Trade war against our friends, weakening our

economy, our national security, and the entire free world, all while cynically waving the American flag.” — Ronald

Reagan

President Herbert Hoover signed the Smoot-Hawley tariff act on June 17, 1930 despite opposition from Democrats,

protests from foreign governments, and a petition signed by over 1,000 economists (Gerlach). It raised levies by

another ~25% on almost all foreign imports on top of a preexisting average of 38.5% on dutiable imports from the

Fordney-McCumber Tariff of 1922 (Kaplan).

The policy had the goal of protecting domestic US industries, especially the agriculture sector. Contrary to

nation-wide economic prosperity during the Roaring Twenties, average farm incomes declined from 1920 to 1929. While

his initial pledge during the election campaign focused on tariffs for agricultural products, the policy was

eventually extended due to pressure from business leaders and other Republican party members (O’Brien).

Economists are generally uniform in their criticism of protectionist policies in the form of tariffs.

Theoretically, tariffs do not change capital, labour, or technology, and would therefore have little macroeconomic

impact on indicators such as employment. However, in the short term, with raising the price of imported goods, a

tariff should increase the net export by reducing the total import (M) without any direct effect on total export

(X). Thus, Gross Domestic Product would increase relative to its previous level: GDP is equal to the aggregate

expenditure, which can be calculated by Y = C + I + G + (X - M). This underpins logic behind protectionist tariff

policies such as Smoot-Hawley, which sought to ameliorate falling investment and consumer spending during economic

downturns.

Nevertheless, an essential postulate of the previous analysis is that there is no significant retaliation by

trading partners that would negatively affect US exports. In the case of Smoot-Hawley, Canada, Cuba, Mexico, France,

Italy, Spain, Argentina, Australia, New Zealand, and Switzerland all imposed retaliatory tariffs. American exports

fell by an average of 31% to these countries (Mitchener). The exact effects of these retaliatory measures are hard

to pinpoint, as they amplified an already plunging global trade during the Great Depression. One thing is certain:

the tariff didn’t work out how the Hoover administration would have liked it to.

“I am a Tariff Man. When people or countries come in to raid the great wealth of our Nation, I want them to pay

for the privilege of doing so. It will always be the best way to max out our economic power. We are right now taking

in $billions in Tariffs. MAKE AMERICA RICH AGAIN” — Donald Trump

Despite the official US Senate website referring to the Smoot-Hawley tariff act as being “among the most

catastrophic acts in congressional history”, Trump commended it but stated that it was too late (“The Senate”). On

the 2nd of April, Trump imposed his own set of sweeping tariffs, ranging from 10% on the United Kingdom to 49% on

Cambodia.

Within days of the policy, a global trade war has already begun. China has recently capped its retaliatory tariffs

at 125%, calling tariff strategies from the White House “a joke”. The EU imposed 25% retaliatory tariffs, although

this was suspended for negotiations after Trump reduced US duties from 20% to 10%. Other global leaders which did

not retaliate reprimanded this policy, with Australian Prime Minister Anthony Albanese stating that the tariffs

“have no basis in logic” and that they are “not the action of a friend”.

The tariffs disrupted global economies and assets as soon as they were announced. $10 trillion USD in global equity

value was wiped out over three days, with the S&P 500 suffering its worst losses since its creation in the 1950s.

Crude oil prices dropped below $60 per barrel, lowest since 2021. Bitcoin fell by 30% since Trump’s inauguration

(Chughtai). Interest rates for US Bonds, usually a safe asset for investors, have increased due to higher

uncertainty and perceived risk.

Perhaps intimated by political backlash and harsh economic statistics, Trump has currently suspended all reciprocal

tariffs aside from ones placed on China. He has even exempted smartphones and computers from China from tariffs, its

biggest export to the United States. Conflicting with the policy objective of moving high-tech productions to the

US, this was likely due to pressure from tech giants such as Apple and Nvidia.

“We call a tariff a protective measure. It does protect; it protects the consumer very well against one thing.

It protects the consumer against low prices.” — Milton Friedman

There is a fundamental difference between the Smoot-Hawley act and the Trump tariffs of 2025, which lies in their

purpose. The Smoot-Hawley tariff act is one to reduce domestic unemployment, and Trump’s biggest objective is to

“stop other countries from robbing the United States of America” with the reduction of trade deficits. Regardless,

both have caused slowing global trade and negative effects on US and foreign economies. We already know the

historical result of the Smoot-Hawley; the policies from Donald Trump have been and remain extremely unpredictable.

Only time will tell the long-term ramifications that arise from the political chaos of 2025.

This article is up-to-date as of April 19th, 2025.

Chughtai, Alia, and Mohammed Haddad. "Eight charts that reveal the economic impact of Trump's tariffs." Al

Jazeera, 9 Apr. 2025,

www.aljazeera.com/economy/2025/4/9/eight-charts-that-reveal-the-economic-impact-of-trumps-tariffs.

Gerlach, Stefan. "When protectionism backfired: The Smoot-Hawley Tariff Act of 1930." EFG,

www.efginternational.com/us/insights/2025/when_protectionism_backfired_the_smoot-hawley_tariff_act_of_1930.html.

Kaplan, Edward S. "The Fordney-McCumber Tariff of 1922." Economic History Association, EHA,

eh.net/encyclopedia/the-fordney-mccumber-tariff-of-1922/.

Mitchener, Kris James, et al. "The Smoot-Hawley Trade War." The Economic Journal, vol. 132, no. 647, 1 Feb. 2022,

pp. 2500-33, https://doi.org/10.1093/ej/ueac006.

O'Brien, Anthony. "Smoot-Hawley Tariff." Economic History Association, EHA,

eh.net/encyclopedia/smoot-hawley-tariff/.

"The Senate Passes the Smoot-Hawley Tariff." United States Senate, The Senate Passes the Smoot-Hawley Tariff.

How did the implementation of Trump’s tariffs on imports affect global trade dynamics, and what are the

potential consequences for global economic stability and recession?

Athena Yip

“The biggest loser of this is definitely the U.S. itself,” says Yuan Mei, assistant professor in the School of

Economics at Singapore Management University.

“It will be difficult for the U.S. to avoid a recession if the tariffs stay at the level that’s been announced,”

Claudia Sahm, chief economist at New Century Advisors, recently told TIME (Jeyaretnam).

Both economists are referring to the same thing, the new tariffs announced by President Trump after his reelection

in 2025 (Jeyaretnam). Economist worldwide seems to believe the biggest victim of tariffs is the United States

herself. The Americans are all at risk of raised tax. Taxing all imports will lead to significant cost for local

businesses which means increased price for local consumers, bringing the United States into a recession and a

sustained economic decline.

A nation-wide recession in the United States undoubtedly will affect economies worldwide. Last week, J.P. Morgan

increased its forecast of the global economy entering a recession by year-end from 40% to 60% (Jeyaretnam). The

effects of the tariffs is described as “a dampening of global demand and production” in both the US and around the

world, according to Ja-Ian Chong, associate professor of political science at the National University of

Singapore.

There are two outcomes off the tariffs. American importers will either choose to absorb the cost or pass on some or

all the cost onto Ameircan consumers (Jeyaretnam). If they choose the first, their profitability decreases which

would lead them to change their cost structure, for example, downsizing operations or firing workers. Though most

likely, they would choose the second causing consumers to tighten their spending habits and resulting in decreased

demand both American and foreign, even possibly resulting in layoffs. Kristina Fong, an economic affairs researcher

at Singapore-based think tank ISEAS-Yusof Ishak Institute’s ASEAN Studies Center says “Basically, you will be

impacted in several ways, no matter how you look at it.”

Not only are countries who directly import to U.S. are affected, others in the production chain are too. Most

products aren’t made and assembled in one country, they use components imported from several places (“The Impact of

Trump’s Proposed Tariffs.”). With a lower demand in the US, goods do not move into the country, the demand for

components that goes into assembling them will also decline. For countries that decide to retaliate against U.S.

tariffs such as China, demand of products from the U.S. would decline, therefore producers of the components used to

make the product would also be impacted (Lawder).

During Trump’s first term, trade tension had pushed firms located in China who still wants to maintain a stable

relationship with U.S. consumers to relocate to other parts of the world (Lawder). Southeast Asia benefited

significantly from this change and American consumers didn’t feel impacted. However, there will be a broader effect

this time given the fact that tariffs had been announced worldwide. Vietnam, Cambodia and Bangladesh were hit with

46%, 49% and 37% tariffs respectively. All 3 countries will face significant economic strain since they export

heavily to the U.S. Last year, Bangladesh exported $7.34 billion worth of goods to the U.S., it’s top export

destination. Vietnam is equally at risk, manufacturing 50% of Nike’s footwear and 39% of Adidas. OCBC estimates it

could lose over 40% of total exported goods due to high tariffs, which may lead some to relocate their factories or

even decreased investments in the country (Zandt).

According to Ivan Png, an economist at the National University of Singapore, the U.S. tariffs could affect prices

for consumers outside of the U.S. with major exporters such as China redirecting their exports to other countries

that set lower tariffs. If true, production will remain high and prices will be changed to appeal to smaller

markets. This will lead to disruptions to the global supply chain could in turn lead to unintended

consequences such as increased production costs that may be passed onto consumers. Despite the possible

consequences, many counties have began diversifying their trade patterns and engaging with “more reliable” trading

partners such as China (News, PBS). Others have rushed to negiosiate with Trump with the hopes of reducing negative

economic effects. Vietnam, recently hit with 46% tariff offered to bring its tariff on U.S. products down to none

at all though the U.S. still refused the deal (News, PBS). Clearly, removing or reducing tariffs on the U.S. isn’t

enough for Trump, he wants the countries to buy close to equal the amount of U.S. goods as the U.S. buys from

them.

Many criticise this approach. “These tariffs will not produce that,” Menon says. “Nothing will produce that,

because that’s not what trade is about. The way to balance your trade is not to trade at all. You trade with

countries because they do things differently and with different costs and prices than you can.” Even if Trump

ultimately backs down and reverses or lowers many of the tariffs he’s levied on the world, to some extent, Menon

says, the damage has already been done. “In a matter of a few months, the U.S. has thrown away decades of goodwill

with its allies by taking on this kind of ludicrous stance. When you come out and start penalizing your friends with

tariffs based on a nonsensical formula… there’s no turning back.”

The implementation of Trump’s tariffs had already began reshaping global trade dynamics. The repercussions of these

tariffs span from immediate cost to American consumers and businesses to global supply chains, potentially even

triggering widespread economic instability. The long term effects on international relations and economic

partnerships may lead to a reconfiguration of global trade networks and lasting implications for economy worldwide.

The path forward depends greatly on the ability of nations to navigate these challenges and find common ground.

Works Cited

Jeyaretnam, Miranda. “How Trump’s Tariffs Could Lead to a Global Recession.” TIME, Time, 9 Apr. 2025,

time.com/7275987/trump-tariffs-global-economy-recession-trade-war-asia-world-impacts/. Accessed 12 Apr. 2025.

“The Impact of Trump’s Proposed Tariffs.” ITEP, 2024, itep.org/trump-tariffs-tax-increase-impact/. Accessed 12

Apr. 2025.

Lawder, David. “Trump Upended Trade Once, Aims to Do so Again with New Tariffs.” Reuters, 16 Jan. 2025,

www.reuters.com/markets/us/trump-upended-trade-once-aims-do-so-again-with-new-tariffs-2025-01-16/. Accessed 12

Apr. 2025.

News, PBS. “Analysis: The Potential Economic Effects of Trump’s Tariffs and Trade War, in 9 Charts.” PBS News, 2

Feb. 2025,

www.pbs.org/newshour/economy/analysis-the-potential-economic-effects-of-trumps-tariffs-and-trade-war-in-9-charts.

Accessed 12 Apr. 2025.

Zandt, Florian. “Infographic: Trump Tariff Plans Would Hit Most Important Trade Partners.” Statista Daily Data,

Statista, 29 Jan. 2025,

www.statista.com/chart/33851/countries-with-the-highest-value-of-good-imported-into-exported-from-the-us/.

Accessed 12 Apr. 2025.

Is History Repeating Itself? A Comparison of Trump’s Tariffs and the Smoot-Hawley Incident

Amy Liu

“Those that fail to learn from history are doomed to repeat it” — Winston Churchill

It started with the forgotten depression that lasted from January to July in 1921. The US stock market dropped

significantly, and corporate profits plummeted. Unemployment surged to remarkable levels, especially in comparison

to the previous war period. In the aftermath of that war, the US faced a tricky transition. Factories shut down, and

many soldiers returned home to flood the workforce. Inflation soared. In response, the government cut spending

drastically and hiked interest rates sharply. The result was a severe collapse in industrial production, the worst

recorded at the time. Prices plunged, leading to mass business failures and leaving millions struggling to

survive. The real turnaround came when the federal government cut government spending by 65% from 18.5 billion to 6

billion. This helped stabilize the economy and eventually fueled growth in the Roaring 20s. By the spring of 1921,

President Warren G Harding had taken over, marking a period of changes back to higher tariffs.

Protectionism refers to government policies that restrict international trade: limit imports, allowing domestic

industries a better chance to thrive. Tariffs are the most common means of restriction. They serve as taxes on

imported goods, making foreign products pricier and encouraging local purchases. America's early days were heavily

marked by protectionism, but in the late nineteenth and early twentieth centuries, the country experienced a phase

of relatively free trade, prompted by the Underwood-Simmons tariff of 1913 that lowered tariffs and introduced an

income tax. However, WW1 shot the US back into protectionism. Once WW1 ended, Europe’s economy was recovering, and

US industries had competition as the farmers who sold crops to Europe during the war were losing the market as

Europe’s agricultural industry was rebounding.

A significant turning point came in 1922 with the Fordney McCumber Tariff, which raised tariffs much higher than

previously seen. This law also allowed the president to adjust tariffs significantly to balance domestic and foreign

production costs, aiming to protect US industries from competition. However, this tariff had consequences, as it

crippled European exports to the US and heightened global tensions. War-torn nations found it challenging to repay

debts, deepening the crisis instead of aiding global recovery. Meanwhile, tariffs in the US climbed through the

following decade, distorting the international trading landscape.

The 1920s emerged as a decade of wild growth in the US—an era marked by extraordinary consumerism. People poured

money into stocks, driving prices to dizzying heights. However, the market was unsustainable, and it was poised for

a dramatic crash. Everything changed in October when the stock market began its catastrophic decline. This marked

the onset of widespread panic and resulted in an irreversible loss of value across the market.

As the market collapsed, everything else soon followed. The economy froze, banks failed, and businesses went

bankrupt, resulting in mass unemployment. Consumers, witnessing their wealth evaporate, halted spending. Factories

and stores closed, bringing the entire nation to a standstill. Farmers, already grappling with post-war

overproduction, faced plummeting crop prices and unmanageable debts. Then came a fateful decision from the

government.

President Herbert Hoover, under pressure, decided to sign the Smoot-Hawley Tariff Act into law in 1930. The bill

was originally meant to help struggling farmers by raising duties on agricultural imports. But it didn’t stay that

simple. Various industries saw an opportunity and lobbied for tariffs on all sorts of products. By the time the bill

was passed, it was a full-scale tariff hike on over 20,000 foreign goods.

Soon, various countries retaliated with their tariffs aimed directly at US goods, initiating a trade war that

escalated tensions globally. The largest trading partner at the time, Canada, with 18% of all exports going to

Canada and receiving 11% of Canada’s responded, aiming to protect its economy. Canadian Prime Minister at the time,

William Lyon Mackenzie King, slapped tariffs on just 16 American products. But when RB Bennett took over in 1930, he

cranked up the pressure. Canada raised tariffs even further on US goods while simultaneously cutting tariffs on

roughly 270 products from the United Kingdom and its dominions. By 1932, Canada hosted a massive trade summit with

the other British territories, laying the groundwork for a trade bloc that actively excluded the US.

Canadian exports to the UK surged, especially in agriculture. The very industry Smoot-Hawley was meant to protect.

But this was just the start. A total of 25 countries would eventually strike back with tariffs of their own.

Countries already struggling from the Great Depression suddenly faced even higher barriers to selling goods to the

US, making an already bad situation worse. US exports to retaliating nations fell by 28 to 32%. Even countries that

didn't retaliate still cut US exports by 15 to 23%. Global trade collapsed, dropping by 66% between 1929 and

1934.

How do Trump’s proposed tariffs impact long-term GDP growth in the US?

Eason Huang

Figure 1. Donald Trump’s Announcement of the Tariff (Bloomberg Law).

A. Background Information

On April 2, 2025, Trump declared a national state of emergency to address what he called the "huge and persistent

US trade deficit", announcing his most expensive tariff plan. Under the justification of the “Make America Great

Again” and “America First” agenda, he enacted a series of protective tariffs based on a baseline 10 percent tariff

on all nations. More importantly, Trump escalated the trade war with China, imposing import taxes of 145% on Chinese

goods exported into the US (Huld).

As early as Trump’s first presidency, between 2017 and 2021, he had already advocated for protective tariffs as a

tool to regulate trade and commercial activities with foreign nations. As a conservative president, Trump

prioritizes the US’s benefits and believes that the protective measures could encourage US consumers to purchase

US-made products ("Trade wars").

Until the draft of this essay (2025 September), Trump has imposed and suspended the tariffs several times. The

latest tariff took effect after midnight on Aug. 7, targeting nearly all US trading partners (Minsberg).

The protective tariff is typically viewed as a tool to protect domestic businesses. Such a tariff aims at

revitalizing the domestic economy. However, would the tariff with a significantly high rate damage the US economy?

The answer is YES — the tariffs would hobble the US economy through supply chain disruptions and

supply chain

turbulence.

B. Higher Prices and Supply Chain Disruptions

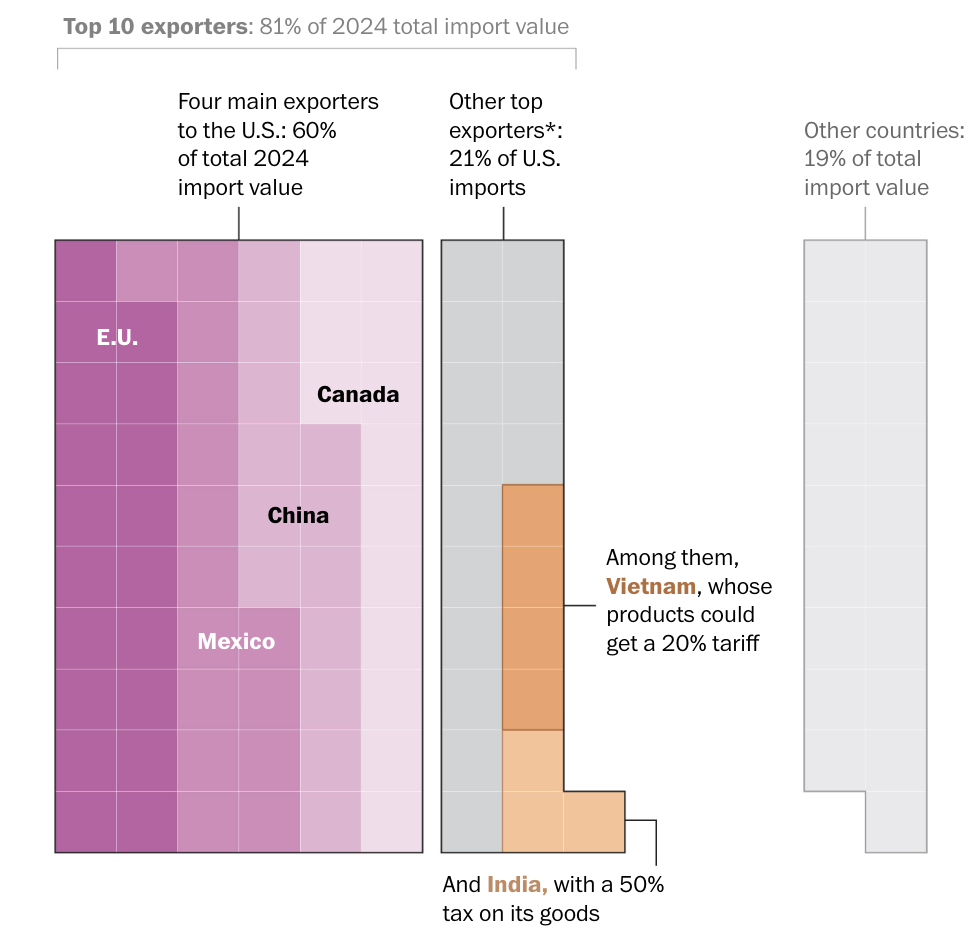

Figure 2. Top Suppliers to the US (The Washington Post).

The tariff policy initially leads to a higher price of goods in the US domestic market. As shown in Figure 2, over

the past decades, the US economy has had a strong reliance on Mexico, Canada, China, and the EU. They “sent almost

$2 trillion into the country last year, or about 60 percent of all imports by value”, according to the Washington

Post (Lerman and Melgar).

By levying a higher tax on imported goods, people need to pay more for the imported goods. The impact is apparent

because, given that their income is constant, they have lower purchasing power. Each American household needs to pay

more — $2,400 per year — according to estimates from the Budget Lab at Yale University (Sonnenfeld and

Henriques).

To compensate for this, consumers are forced to cut their consumption of leisure and entertainment. This

contraction in demand subsequently depresses revenues and profits for domestic service industries, forcing them to

reduce hiring and cut the hours of employees. Ultimately, the prolonged demand downturn can lead to permanent

disclosures, negatively affecting the long-term GDP.

Meanwhile, businesses also face higher production costs and increased competition. Taking imported semiconductors

as an example, Trump imposed a 100% tariff for the sake of attracting providers, such as TSMC, to invest in US

manufacturing (Shalal and Shepardson). Apple, for example, depends on advanced imported chips, including the A18, M4

chip, etc. High prices can then be a block to the supply chain, causing delays and uncertainty. Of course, this

increase in input costs will squeeze the profit. Businesses have to pass the expense on to consumers through higher

retail prices. However, this creates a vicious cycle: though consumers have already been strained by the direct

burden of tariffs, they now face even higher prices for domestic goods. Their purchasing power is diminished

further, cutting their consumption and investments. Ultimately, this will deepen the economic strain.

As such, rather than attracting investments and incentives in US manufacturing, tariffs could impede consumers’

consumption of domestic services and mess up businesses, causing turbulence in the domestic market.

C. Export Declines

Figure 3. US Ports in Portland (Inbound Logistics).

Contrary to Trump’s claim, tariffs actually hurt US exporters by making American goods more expensive and less

competitive abroad. Other countries also propose their retaliatory tariff plan, and in this case, they seek to “take

revenge” against the US exported goods. For example, the US placed 145% tariffs on Chinese goods. In response, China

retaliated with 125% tariffs on US goods (Cash and Zhang).

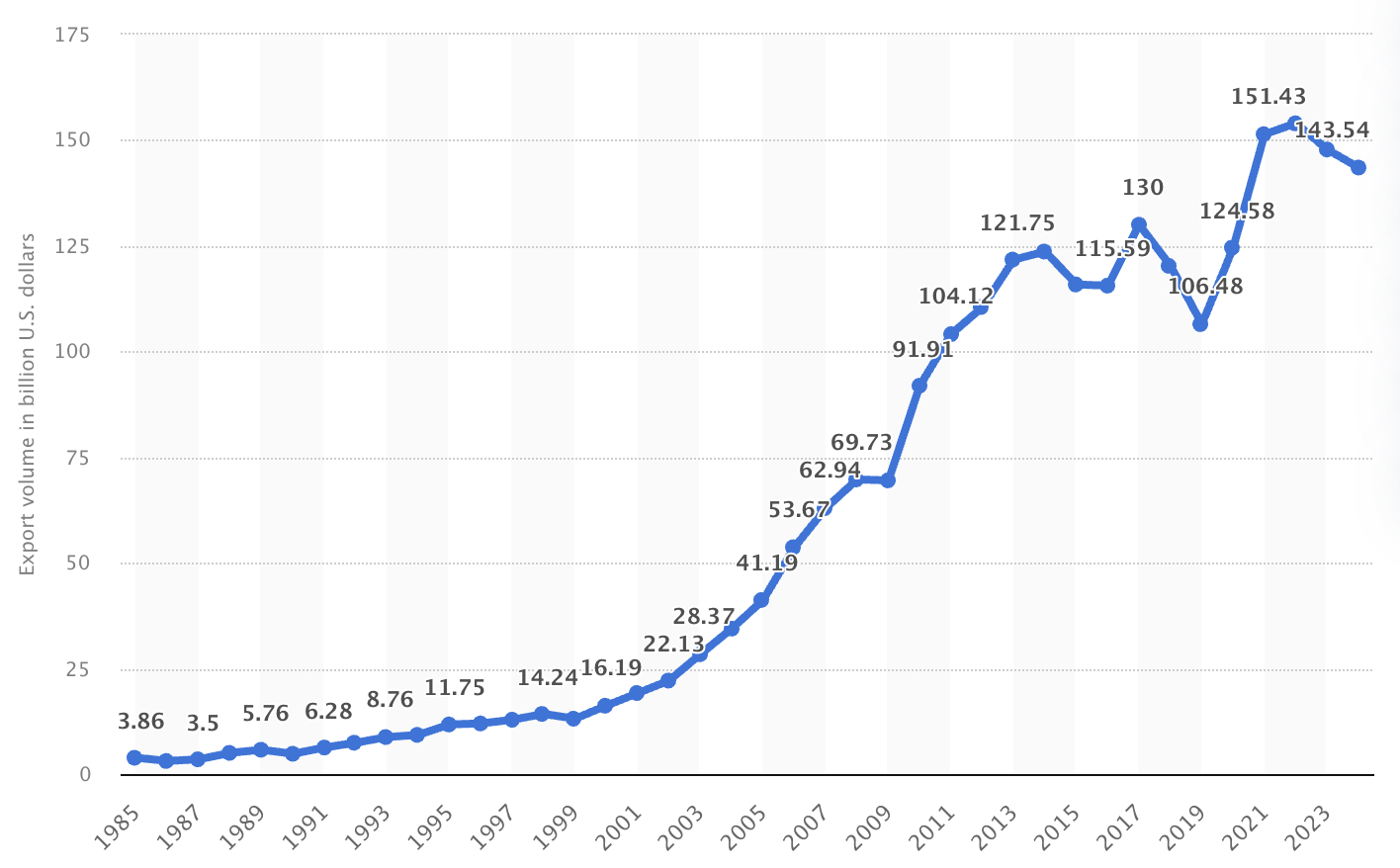

Figure 4. US Exports to China 1985 to 2024 (Statista).

This makes the US exports significantly more expensive for consumers and businesses in China. According to

Statista, the US’s exports have shown a steady, growing upward trend from 1985 to 2024 (shown in Figure 4). However,

a sharp increase in exported goods could hinder this growth. Demand for US goods falls, “US agricultural exports to

China dropped nearly 40% in the period from June 2024 to June 2025,” according to IDN Financials (Hannany and

Priambodo).

How would this impact US GDP? It is a consensus that the GDP of a country is calculated as:

consumption + investment + government spending + (exports - imports)

A fall of 40% drop in exports to China will drag down GDP in the short term. In terms of the long-term effect, the

retaliatory tariff disrupts the global supply chain, creating an issue for both US businesses that “goods expected

to arrive in the next six to eight weeks simply won’t” (Confino). Indeed, this fluctuation will result in a

reduction in profitability. As time goes on, this will engender a recession in economics.

For the US exporters, they also face a hard time. The exports saw a fall at more than 21 major US ports, including

the Port of Portland (-50%) and Los Angeles (-17%) (Confino). As these goods are now remaining in the US, giving

rise to a disruption to supply chains. As a consequence, the US will gradually lose global market share, and it is

extremely difficult to win the market share back again. Eventually, the US will be isolated from global markets and

have fewer goods to export, shrinking the potential market for the US. All in all, a sustained, long-term GDP will

be profoundly damaging.

D. Historical View

The future is full of possibilities and changes, but having a close look at history will provide a clearer picture

of the tariff consequences. 100 years ago, the US suffered drastically after President Herbert Hoover enacted a

series of tariff plans. At that time, Hoover signed the Smoot–Hawley Tariff Act of 1930 in an attempt to attract

voters, especially the farmers. He promised that the tariff act could protect domestic agriculture from

competition.

However, this policy went contrary to his wishes. Right after the stipulation, Canada, the EU, and many other

countries retaliated by imposing their own high tariffs on US goods. Canada, for example, strengthened its ties with

the UK, aiming to fight against the US’ tariff. Moreover, the US saw a 65% decline in its exports, which fell from

about $7 billion in 1929 to just $2.5 billion in 1932.

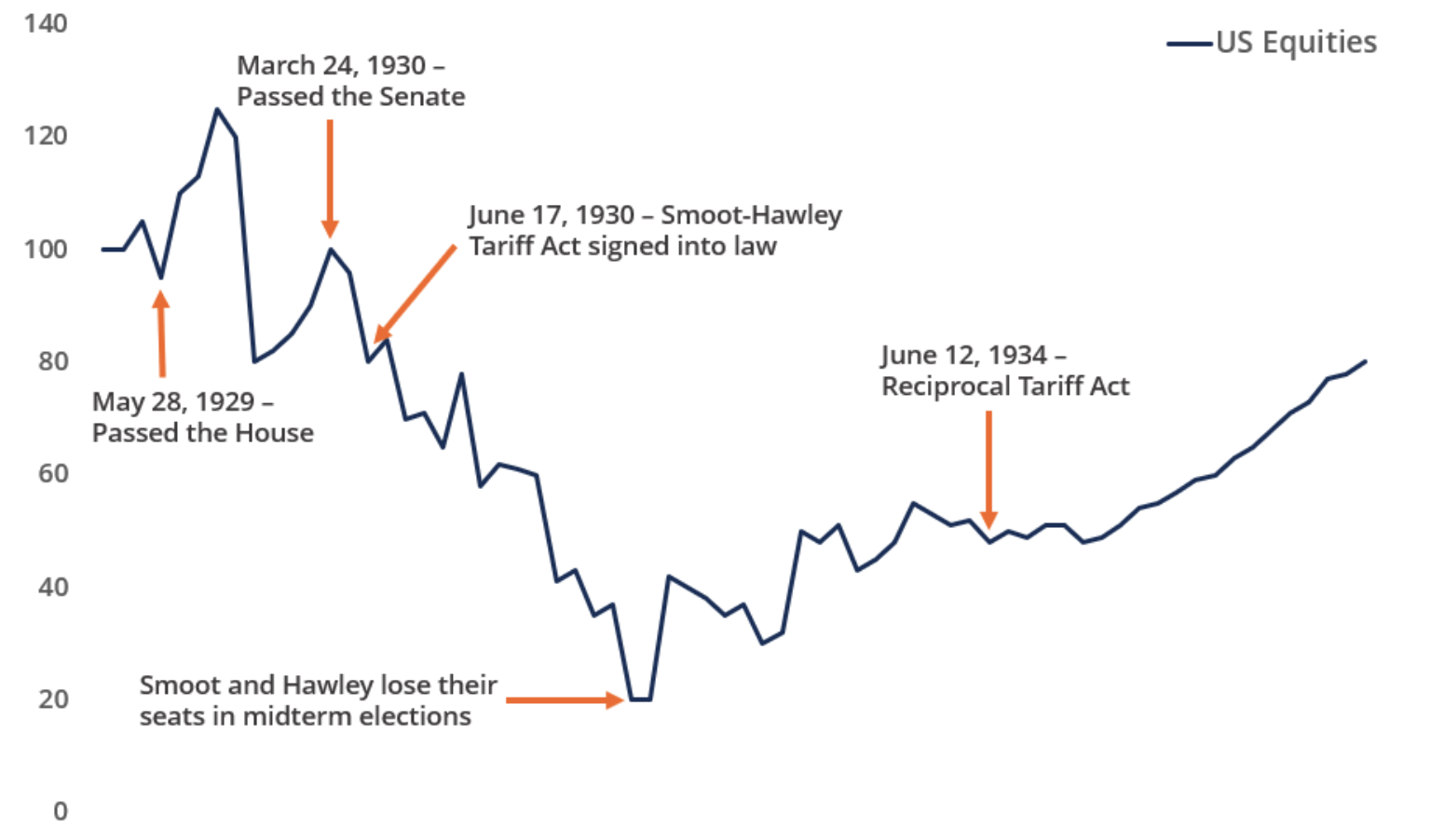

Figure 5. Impact of Smoot–Hawley Tariff Act on US Equities (CFI).

The situation of equities also reflects the struggling economy. As shown in Figure 5, immediately after the

enactment, the equities dropped dramatically from 80 to 20. The equities finally recovered not until the passing of

the Reciprocal Tariff Act by President Franklin Roosevelt ("Smoot-Hawley Tariff").

According to economist Douglas Irwin, the act exacerbated the Great Depression and caused long-term economic

disruptions. President Reagan also criticized that the Smoot–Hawley Tariff Act “greatly prevented the economic

recovery…eventually occurs is the first own-grown industries start relying on government protection of high tariffs,

and stop competing and stop making innovative management and technological changes to succeed in the world market”

(President Reagan's).

E. Conclusion

As the essay has argued, such tariff policy is a self-defeating economic strategy, engendering severe damage to the

US economy. The immediate consequences are higher prices for consumers and increased production costs for

businesses. This leads to reduced purchasing power and supply chain turbulence, undermining the long-term GDP

growth

Furthermore, the retaliatory tariffs could mutilate US exports, as evidenced by the historical 65% decline and 40%

drop in exports to China. This impact on both imports and exports marks a drag on GDP by disrupting global supply

chains and precipitating a prolonged economic downturn. Therefore, the evidence clearly shows that far from making

“America Great,” such extreme protective tariffs would backfire. It will likely limit the US GDP growth.

Of course, the prediction of the future is not 100% accurate, but what we learned from the Smoot-Hawley Tariff Act

already gives us a stark warning.

Works Cited

Cash, Joe, and Yukun Zhang. "China raises duties on US goods to 125%, calls Trump tariff hikes a 'joke.'"

Reuters, 11 Apr. 2025,

www.reuters.com/world/china/china-increase-tariffs-us-goods-125-up-84-finance-ministry-says-2025-04-11/. Accessed

21 July 2025.

Confino, Paolo. "Trump's tariffs have reportedly caused an up to 50% plummet in exports at some ports, and goods

expected to arrive in the next month 'simply won't.'" Fortune, 6 May 2025,

fortune.com/2025/05/06/trump-tariffs-exports-plummet-ports/. Accessed 26 Aug. 2025.

"Fact Sheet: President Donald J. Trump Modifies the Scope of Reciprocal Tariffs and Establishes Procedures for

Implementing Trade Deals." The White House, 5 Sept. 2025,

www.whitehouse.gov/fact-sheets/2025/09/fact-sheet-president-donald-j-trump-modifies-the-scope-of-reciprocal-tariffs-and-establishes-procedures-for-implementing-trade-deals/.

Accessed 7 July 2025.

Hannany, Zetta, and Dhika Priambodo. "Trump tariffs trigger 40% plunge in US agricultural exports to China." IDN

Financials, 28 Aug. 2025,

www.idnfinancials.com/news/56883/trump-tariffs-trigger-40-plunge-in-us-agricultural-exports-to-china. Accessed 31

Aug. 2025.

Huld, Arendse. "Trump Raises Tariffs on China to 145% – Overview and Trade Implications." China Briefing, 11 Apr.

2025, www.china-briefing.com/news/trump-raises-tariffs-on-china-to-145-overview-and-trade-implications/. Accessed

7 July 2025.

Lerman, Rachel, and Luis Melgar. "See where Trump's tariffs are driving up prices on household items for now."

The Washington Post, 4 Sept. 2025,

www.washingtonpost.com/business/2025/09/04/trump-tariffs-imports-products-prices/. Accessed 7 Sept. 2025.

Minsberg, Talya. "A Timeline of Trump's On-Again, Off-Again Tariffs." The New York Times, 13 Mar. 2025,

www.nytimes.com/2025/03/13/business/economy/trump-tariff-timeline.html. Accessed 2 Sept. 2025.

President Reagan's Radio Address on Free and Fair Trade on April 25, 1987. YouTube,

www.youtube.com/watch?v=5t5QK03KXPc. Accessed 28 Aug. 2025.

Shalal, Andrea, and David Shepardson. "Trump says US to levy 100% tariff on imported chips, but some firms

exempt." Reuters, 8 Aug. 2025,

www.reuters.com/world/china/trump-says-us-levy-100-tariff-imported-chips-some-firms-exempt-2025-08-07/. Accessed 1

Sept. 2025.

"Smoot-Hawley Tariff Act." CFI, corporatefinanceinstitute.com/resources/economics/smoot-hawley-tariff-act/.

Accessed 14 Aug. 2025.

Sonnenfeld, Jeffrey A., and Stephen Henriques. "Trump's Tariff Tantrums Are Hobbling the U.S. Economy." Yale

Insights, 11 Aug. 2025, insights.som.yale.edu/insights/trumps-tariff-tantrums-are-hobbling-the-us-economy.

Accessed 18 Aug. 2025.

Tierney, Abigail. "Value of U.S. exports of trade goods to China from 1985 to 2024." statista, 6 May 2025,

www.statista.com/statistics/186510/volume-of-us-exports-of-trade-goods-to-china-since-1985/. Accessed 20 Aug.

2025.

"Trade wars, Trump tariffs and protectionism explained." BBC News, 11 May 2019, www.bbc.com/news/world-43512098.

Accessed 3 Aug. 2025.

How has Trump’s planned withdrawal of EV subsidies affected car producers?

Thomas Wu, Samson Suen

The planned withdrawal of electric vehicle (EV) subsidies under the Trump administration has complex implications

on the EV market. Initially the demand side subsidy, of $7500 tax credits for EV’s under $80000, this subsidy

positively increased sales across multiple brands. For example, with General motors (GM) its sales were reported by

21% increase in sales, while other manufacturers such as Honda, Hyundai, and Nissan each saw 10% growth in sales

(Boudette, 2025).

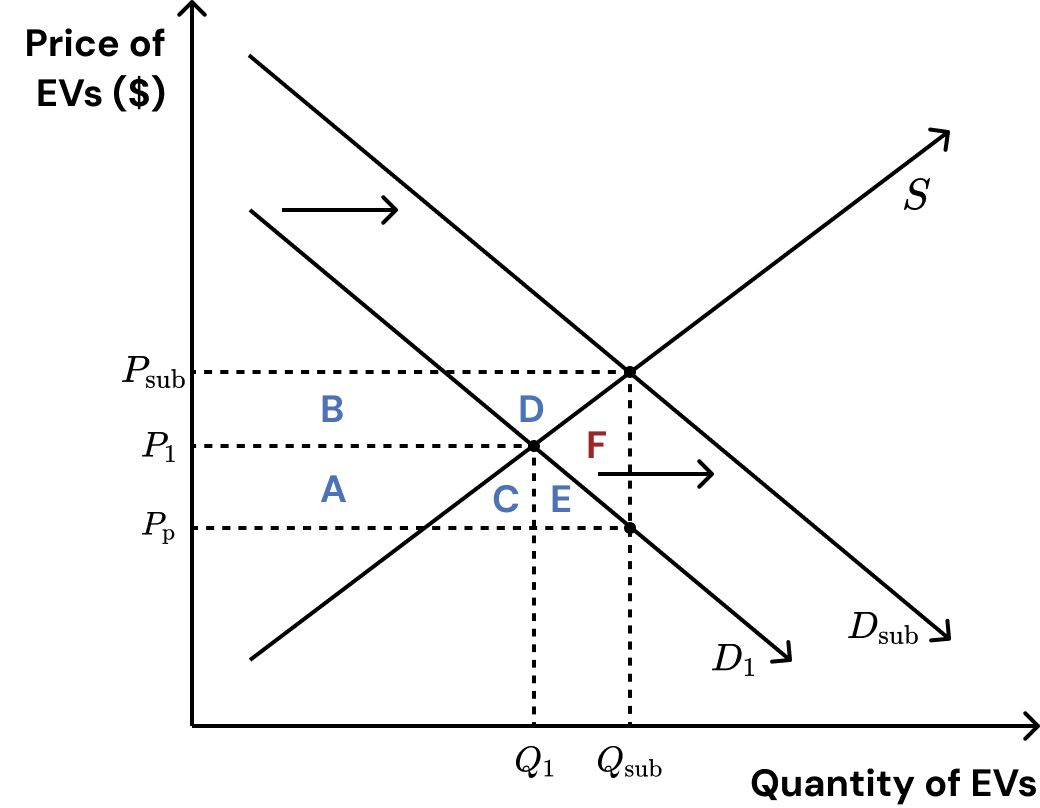

Figure 1: Effect of demand side subsidies.

The subsidy, funded by the US government, as shown by area (A, B, C, D, E, F in Figure 1), shifts the demand curve

from the right (from Q1 to Qsub) reflecting the increase in EV sales which is supported by the

previous data. By incentivising consumption of EVs a merit good (as it reduces the consumption of fossil fuels

vehicles) mitigating negative externalities in the form of pollution, which inflict additional costs on society. As

illustrated by the data and the graph this leads to increased sales and revenue for EV producers.

However, this subsidy carries an opportunity cost, the allocated funds (A, B, C, D, E, F) could have been diverted

to alternate public investment such as infrastructure development. Additionally, given the US’s severe national

debt, continued subsidies risk widening budget deficits exacerbating debt levels. Additionally, using demand side

policies result in a deadweight loss (area F), causing the loss of allocative efficiency within a market.

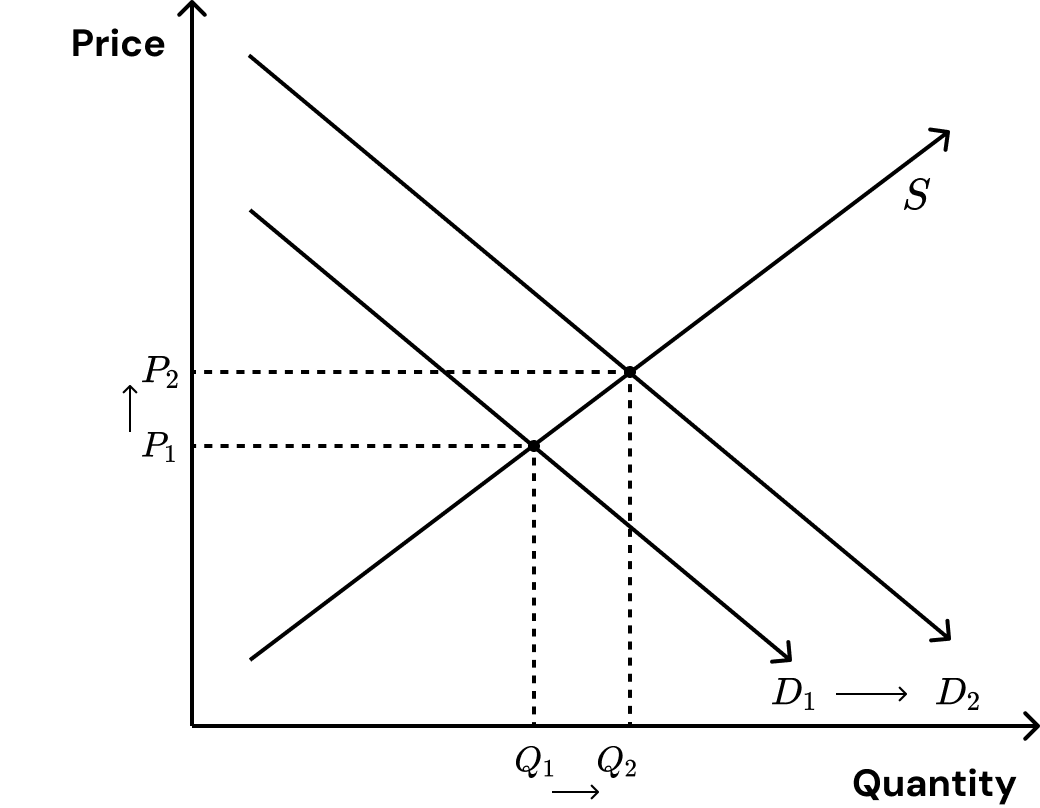

Figure 2: Market for EVs after announcement of withdrawal of subsidies in U.S.

The withdrawal of subsidies will increase the effective cost of EVs. Therefore, in anticipation of the increase in

costs, demand will increase in the short run as consumers may decide to purchase an EV before the withdrawal of the

subsidies to take advantage of the tax credits. This is demonstrated in Figure 2, where demand shifts right from

D1 to D2 in the short run, resulting in an increase in price and quantity from P1

to P2 and Q1 to Q2, respectively.

However, in the long run, when the subsidies have been withdrawn, the effective cost of EVs will increase as

consumers no longer receive the tax credits as a benefit. As depicted in Figure 2, demand shifts left from

D1 + subsidy to D1 due to consumers opting out. Following the increase in price from

P1 to P2, consumers may choose substitute goods of EVs, such as fossil fuel vehicles, which

may be cheaper.

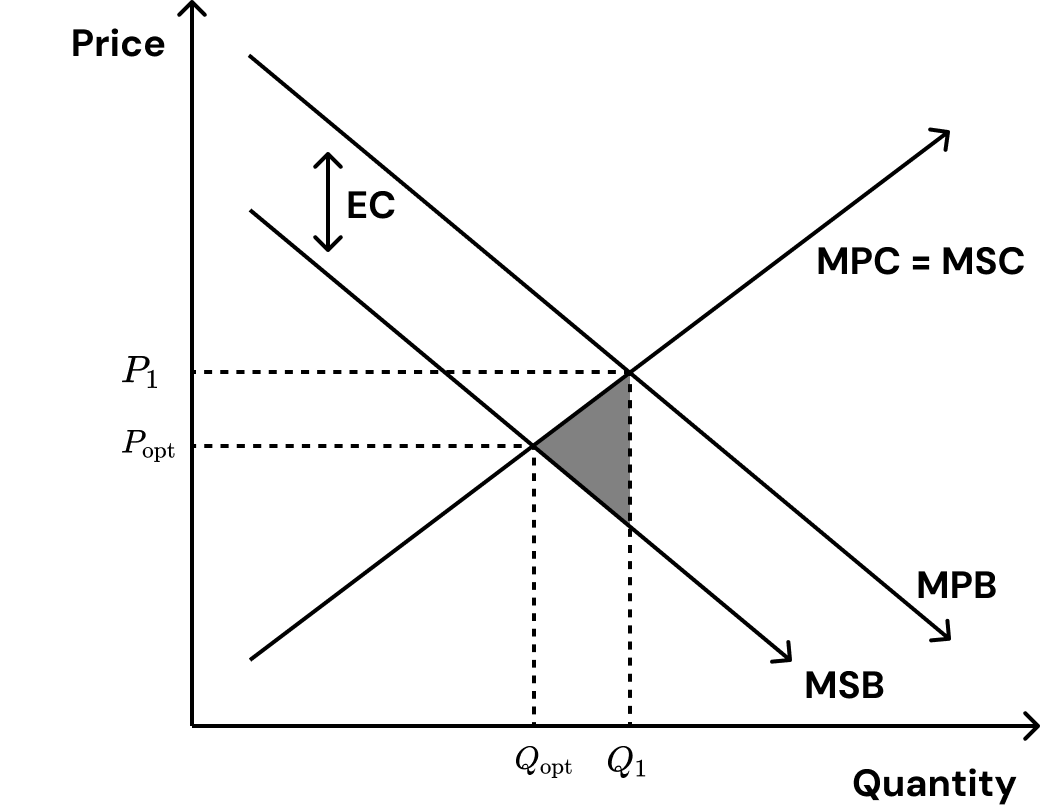

Figure 3: Market for fossil fuel vehicles.

An increase in demand for fossil fuel vehicles raises another issue: sustainability. Fossil fuel vehicles are the

largest contributor to greenhouse gas emissions in the US, accounting for 28% (United States Environmental

Protection Agency). As such, fossil fuel vehicles have negative externalities of consumption, in which using them

results in external costs, such as the worsening of the global warming crisis. This is demonstrated in Figure 3,

where marginal social benefit (MSB) is less than marginal private benefit (MPB), resulting in the previously

mentioned external cost and deadweight loss (shaded).

Works Cited

Bloomberg. “Trump Orders Removal of EV-Favoring Policies and Subsidies.” Energy Connects, 21 Jan. 2025,

www.energyconnects.com/news/renewables/2025/january/trump-orders-removal-of-ev-favoring-policies-and-subsidies/.

Accessed 25 May 2025.

United States Environmental Protection Agency. “Carbon Pollution from Transportation.” US EPA, United States

Environmental Protection Agency, 14 May 2024,

www.epa.gov/transportation-air-pollution-and-climate-change/carbon-pollution-transportation.

Boudette, N. E. (2025, January 3). E.V. Demand Leads Automakers to a Strong 2024 Finish. Nytimes.com; The New

York Times. https://www.nytimes.com/2025/01/03/business/ford-gm-vehicle-sales.html

How billionaires pay less taxes using offshore accounts

Joseph Wu

In recent years, the use of offshore accounts by billionaires has garnered significant attention, raising questions

about wealth inequality, tax evasion, and financial transparency. Offshore accounts are financial accounts held in a

country outside of an individual’s residence, often used to minimize tax liabilities and protect assets. This

article explores the implications of this practice, the motivations behind it, and its impact on global

economies.

The Appeal of Offshore Accounts

Billionaires often turn to offshore accounts for several reasons. Primarily, these accounts offer tax advantages.

By placing assets in jurisdictions with lower tax rates, individuals can significantly reduce their taxable income.

Many offshore financial centers, such as the Cayman Islands, Bermuda, and Panama, have established themselves as tax

havens, attracting wealthy individuals seeking to preserve their wealth (Zucman).

Another motivation is privacy. Offshore accounts can provide a level of anonymity that is difficult to achieve with

domestic accounts. This privacy is appealing to billionaires who may wish to shield their financial activities from

public scrutiny (Piketty). Additionally, offshore accounts can offer protection from political or economic

instability in an individual's home country, allowing for greater financial security (Oxfam).

Legal vs. Illegal Practices

It is essential to differentiate between legal tax avoidance and illegal tax evasion. While using offshore accounts

can be legal if all income is reported and taxes are paid according to the laws of one's home country, many

individuals misuse these accounts for tax evasion, which is illegal. This distinction is crucial in discussions

about the ethics of offshore banking.

The Panama Papers leak in 2016 highlighted how some billionaires and public officials exploited offshore accounts

to hide wealth and evade taxes. The revelations led to widespread outrage and calls for greater transparency and

regulation of offshore banking (Baker). In response, some governments have taken steps to crack down on these

practices, increasing pressure on tax havens to comply with international tax standards.

The Impact on Global Economies

The practice of using offshore accounts has far-reaching consequences for global economies. When billionaires evade

taxes, governments lose significant revenue that could be used for public services, infrastructure, and social

programs. According to a report by Oxfam, the loss of tax revenue from wealthy individuals using offshore accounts

could fund essential services that benefit society as a whole (Oxfam).

Moreover, the concentration of wealth in the hands of a few exacerbates economic inequality. As billionaires

accumulate wealth in offshore accounts, the gap between the rich and the poor widens, leading to social unrest and a

decline in overall economic mobility (Piketty). This growing inequality poses a threat to democratic institutions

and social cohesion, as citizens become increasingly frustrated with perceived injustices in the financial

system.

Conclusion

The use of offshore accounts by billionaires is a complex issue that touches on themes of wealth, power, and

inequality. While there are legitimate reasons for utilizing offshore banking, the potential for abuse raises

ethical and legal concerns. As global economies struggle with inequality and underfunded public services, the

conversation around offshore accounts must continue. Stricter regulations and increased transparency are essential

steps toward ensuring that the wealthy contribute their fair share to society.

Works Cited

Baker, Ray. "The Panama Papers: What We Learned." The Guardian, 2016,

www.theguardian.com/news/2016/apr/03/panama-papers-what-we-learned.

Oxfam. "The Inequality Virus." Oxfam International, 2021, www.oxfam.org/en/research/inequality-virus.

Piketty, Thomas. Capital in the Twenty-First Century. Belknap Press, 2014.

Zucman, Gabriel. The Hidden Wealth of Nations: The Scourge of Tax Havens. University of Chicago Press, 2015.

What are the economics and repercussions of China’s electronic vehicle boom?

Sebastian Ng

Throughout the streets of Hong Kong, it has been shocking to see acclaimed European car dealerships such as

McLaren, Ferrari, or Mercedes eminently replaced by the sudden influx of Chinese car dealerships. This notable shift

in a global financial hub like Hong Kong reflects the broader changes found within the global automotive landscape.

More specifically, the growing presence of Chinese EVs and their economic implications for their dominance over such

a propelling market.

Currently, China, the factory of the world, has cemented itself as the world’s largest EV producer and exporter, as

it accounts for 50% of global EV production & sales. However, the foundation was laid out by a forward-thinking

national strategy set in 2009. The government, eager to grow its presence within the industry, recognised that

traditional automakers in the US, Japan, and Europe had a deadlock over vehicles with internal combustion engines.

Rather than attempting to cut through such a colluded market, they decided to heavily emphasize EV development, even

establishing it as a core national strategy. Eager to beat the rest of the world to this market, the government set

ambitious targets, aiming to accelerate the adoption of new energy vehicles (NEVs). Explicitly, their goal was to

reach the production and sales of 500,000 NEVs by 2012, representing 5% of passenger car sales.

The ambitious goals of the Chinese were greatly assisted by their aspiring financial support and subsidy programs.

This included a fund of 10 billion yuan, which allocated grants and discounted loans to incentivise further industry

investment. To stimulate demand, the government implemented substantial buyer subsidies and reimbursements that

reached up to 60000 yuan, significantly reducing the cost of EVs for consumers. Further invigoration was carried out

through exemptions from a 10% sales tax on EV purchases, incentivising the average consumer. This extreme

governmental support has laid the foundation for Chinese manufacturers, BYD, NIO, and Xpeng. The former has shown

strong profitability, doubling its net profits to about 9.15 billion yuan in the first quarter of 2025. Furthermore,

it benefits from strong economies of scale, evidenced by the lowering of unit production costs.

Though this shows to be a daring approach to market success, competing countries would argue that it is

illegitimate. According to the World Trade Organisation (WTO), subsidies that confer an unfair advantage and harm

the industries of other countries should be subject ot countervailing measures, such as tariffs. With the heavy

investments poured into the market by the Chinese government, tensions have risen with other global superpowers,

accusing them of unjust trading, benefiting from unfair advantages due to governmental subsidies. On June 12, 2024,

the European Commission announced tariffs ranging from 17.1% to 38.1% on imported Chinese EVS. Such trade

restrictions have intensified geopolitical tensions between other powers, such as the United States, of whom

increased tariffs of 100% in 2024 and with the Trump administration in 2025, it has risen to over 247%.

The constant strain between China and the West has no doubt been a recurring theme in the past decades or even

centuries. Chin, much like many instances in the past, accuses the European Union, Canada, and the United States of

being discriminatory, aiming to contain China’s prospering economic growth. They in fact have appealed to the WTO,

claiming that rules have been violated, undermining global cooperation.

Due to the implementation of global trade policies such as tariffs and import restrictions, China’s EV industry has

had to recalibrate its subsidisation laws, seeing a slight decrease in market value, as its EV exports to areas such

as the EU has nearly 20%. However, Chinese EV company BYD currently still stands as the world’s top EV producer,

defying the odds of global pressures. The accusations towards China’s EV market, whether discriminatory or

protectionist, stand as a symbol of growing tensions between it and Western competitors. China continues to defend

its actions vigorously, standing against the punishments that would take so heavily away from its forward-thinking

investments.

Works Cited

Boudette, Neal E. “China’s Electric-Vehicle Industry Is Booming. The U.S. and Europe Are Trying to Catch Up.” The

New York Times, 12 July 2023, https://www.nytimes.com/2023/07/12/business/china-electric-vehicles.html.

International Energy Agency (IEA). Global EV Outlook 2023. IEA, 2023,

https://www.iea.org/reports/global-ev-outlook-2023.

Lo, Kinling. “How China Became the World’s Electric Vehicle Giant.” South China Morning Post, 15 Nov. 2022,

https://www.scmp.com/business/china-business/article/3198248/how-china-became-worlds-electric-vehicle-giant.

McKinsey & Company. “China’s Electric Vehicle Market: The Road Ahead.” McKinsey Insights, 2023,

https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/chinas-electric-vehicle-market-the-road-ahead.

Naughton, Barry. The Chinese Economy: Adaptation and Growth. MIT Press, 2021.

Reuters. “China’s EV Subsidies and Policies: A Timeline.” Reuters, 10 March 2024,

https://www.reuters.com/business/autos-transportation/chinas-ev-subsidies-policies-timeline-2024-03-10/.

What impacts will Trump’s tariffs have on inflation, and how will this affect the U.S. economy?

Sofie Tse

Within his first month back in the White House, President Trump has already begun imposing aggressive new tariffs –

particularly on imported goods from Mexico, Canada and China. Many economists warn that these protectionist measures

are likely to result in inflationary pressures, not only on imported goods but good across the entire U.S. economy.

As the import prices increase, domestic producers relying on these goods will face higher production costs, forcing

them to raise prices. At the same time, increased demand for now-more expensive American made products could push

inflation even higher. This conflict mirrors the inflationary spiral of Trump’s 2018=2019 trade wars, when tariffs

added an estimated 0.3 percentage points to annual inflation (Iacurci).

One of the primary reasons behind these protectionist measures is to address trade imbalances, and achieve balance

of payments equilibrium – as they attempt to lower the volume of imports and increase spending on domestic products.

By making foreign goods more expensive, tariffs are intended to shift demand onto domestic produced alternatives,

thus improving trade balance. Another key driver of tariffs would be to act as a shield for domestic industries

against foreign competition, protecting struggling industries that are not able to compete with cheaper imports.

Despite the fact that tariffs may temporarily reduce imports, they do not necessarily ensure a sustainable

improvement in the balance of payments. Retaliatory measures imposed by partners can erode export revenues and

increase the cost of domestic production, which ultimately undermine the benefits of these policies.

These tariffs have already imposed short term impacts such as rising prices on imported goods. The average tariff

rate on all imports will rise from 2.5 percent in 2024 to 16.5 percent—the highest average rate since 1937—under the

Trump tariffs announced for 2025. Tariffs will cause imports to fall by slightly more than $800 billion in 2025, or

25 percent (Penn). These tariffs do not merely affect consumer goods, they also impact goods and raw materials that

U.S. companies rely on for manufacturing. As a result, domestic producers face rising manufacturing costs, which

they

will likely pass on to consumers, thereby contributing to broad-based price increases. This cost-push inflation is

expected to disrupt global supply chains especially for industries reliant on foreign components, such as

automotive, electronics and machinery. While tariffs aim to boost domestic production, expanding U.S. manufacturing

takes time, meaning supply will not be able to immediately keep up with demand – this mismatch will fuel inflation,

especially for goods with few substitutes. Furthermore, as of April 4th 2025, China, Canada, and the European Union

have imposed retaliatory tariffs altogether affecting $330 billion of US exports (Mena). These retaliatory measures

make American goods more expensive abroad, lowering the demand for U.S. exports, and squeezing American farmers,

manufacturers, and exporters – many of whom rely heavily on international markets. The result is a dual setback to

the U.S. economy: higher domestic prices, and reduced revenue from abroad. Moreover, the broader economic

environment

shaped by the imposition of tariffs could lead to a decline in global confidence in the U.S. as a reliable trading,

and investment partner. If these tariffs lead global governments and private investors to perceive the U.S. as

pursuing protectionist policies that destabilise global trade, they may redirect their investments toward other

economies perceived as more stable or cooperative. This could further weaken the U.S. position in global markets, as

its ability to attract foreign capital diminishes.

While analysing the overall impact of these tariffs, it is key to look into the long-term impacts they will have on

the United States. Trump’s tariffs would act like a hidden tax on American consumers and businesses, ultimately

dragging down the economy over time. By raising the prices on imported goods, consumption falls 3.5 percent in 2030,

and over 3 percent in 2054, reflecting a sustained drag on purchasing power (Jones). According to Federal Reserve

Chair Jerome Powell, “We face a highly uncertain outlook with elevated risks of both higher unemployment and higher

inflation,” he said at an event just outside Washington, DC. “While tariffs are highly likely to generate at least a

temporary rise in inflation, it is also possible that the effects could be more persistent.” (Ishai). Moreover, if

businesses respond to prolonged tariffs by reshoring production, the transition could be slow yet costly, keeping

prices elevated for years. Higher production expenses would likely be passed down to consumers, leaving inflation

embedded in the U.S. economy. The prolonged rise in costs for businesses could weaken their competitiveness in

global

markets, discouraging innovation and investment. This could slow overall economic growth, reducing the U.S. ability

to remain a global economic leader. Lastly, the regressive impacts of tariffs could have significant adverse impacts

on the broader economy, by changing consumer behavior and reducing aggregate demand. The reduction in consumer

spending due to the rising prices (even of domestic goods), will heavily impact America’s economic growth. Since

consumer spending is a substantial portion of GDP, a decline in demand for goods and services decreases economic

activity, and will eventually create a drag on growth, as businesses face reduced revenues and are less likely to

invest in expansion or innovation.

Ultimately, while tariffs may temporarily shield certain industries, their long-term economic consequences –

reduced consumption, persistent inflation, and weaker global competitiveness could far outweigh any temporary

protectionist measures. Without the implementation of policies to boost productivity or supply strains, the U.S.

risks entering a prolonged period of diminished economic vitality and higher costs for households and businesses

alike.

Works Cited

Horsley, Scott. “Inflation Is Cooling -- but Trump’s Tariffs Could Upend Things.” NPR, 10 Apr. 2025,

www.npr.org/2025/04/10/nx-s1-5358985/consumer-prices-inflation-trump-tariffs-economy. Accessed 26 Apr. 2025.

Iacurci, Greg. “Tariffs, Trade War Inflation Impact to Be “Pretty Ugly” by Summer, Economists Say.” CNBC, 10 Apr.

2025, www.cnbc.com/2025/04/10/tariffs-trade-war-inflation-impact-to-be-pretty-ugly-by-summer.html. Accessed 26

Apr. 2025.

Ishai Melamede. “Nearly Two-Thirds of Americans Disapprove of Trump Tariffs, with Inflation a Broad Concern:

POLL.” ABC News, 25 Apr. 2025,

abcnews.go.com/Politics/thirds-americans-disapprove-trump-tariffs-inflation-broad-concern/story?id=121123815.

Accessed 26 Apr. 2025.

Jones, Callum. “Trump’s Tariffs Will Likely Mean “Higher Inflation and Slower Growth”, Says Fed Chair.” The

Guardian, The Guardian, 4 Apr. 2025,

www.theguardian.com/us-news/2025/apr/04/trump-tariffs-higher-inflation-slower-growth-fed-chair. Accessed 26 Apr.

2025.

Mena, Bryan. “Jerome Powell Warns on Trump’s Tariffs: High Inflation Could Be Here to Stay.” CNN, 4 Apr. 2025,

edition.cnn.com/2025/04/04/economy/jerome-powell-fed-tariffs-jobs/index.html. Accessed 26 Apr. 2025.

“Today, our cities are flooded with illegal aliens. Americans are being squeezed out of the labor force and

their jobs are taken.” — Donald Trump

As President Donald Trump embarks on his second term in 2025, his administration has unleashed a bold and

polarizing immigration agenda with mass deportations at its core. Promising to expel millions of undocumented

immigrants, Trump’s policies aim to reshape America’s workforce and bolster national security, though instead, they

are sending seismic tremors through the U.S. economy (Bender). From labor-intensive industries such as agriculture

and construction to small businesses and local communities, the removal of a significant portion of the labor force

is poised to disrupt supply chains, drive up prices, and strain economic growth (DePillis). Analysts, including

those at the Brookings Institution, project a potential half-point drop in GDP growth for 2025 alone, while the

Peterson Institute warns of price spikes as high as 9.1% by 2028 (AFP). This article explores the far-reaching

economic ripple effects of Trump’s 2025 deportation policies, debunking misconceptions and revealing how they

intersect with his broader economic strategies to redefine America’s economic landscape.

A. The Role of Unauthorized Immigrants in the U.S. Economy

Estimated at 13 million people, unauthorized immigrants are integral to the U.S. Economy (“Unauthorized Immigrants

Today”). With approximately 10 million workers, they constitute 6% of the U.S. labor force, concentrated in critical

industries (“Unauthorized Immigrant Population”). Nearly 1 million of the 2.5 million farmworkers in the U.S. are

unauthorized, per Migration Dialogue at the University of California, supporting roughly 50% of fruit and vegetable

production (“Can America’s Economy”). In construction, 1.5 million unauthorized workers help keep housing costs

lower, as reported by The Economist (“Can America’s Economy”). Additionally, unauthorized immigrants make up about

7% of hospitality workers, such as restaurant staff and cleaners, based on industry estimates (“The Economic and

Fiscal”).

B. Misconceptions About Immigration and Jobs

Trump’s deportation agenda rests on two flawed assumptions: first, that deporting unauthorized immigrants will

automatically open jobs for U.S. citizens, and second, that the labor market has a fixed number of jobs (The

Economist). At a Wilmington campaign rally, Trump claimed, “Every job produced in this country over the last two

years has gone to illegal aliens” (Bender). His top immigration adviser echoed this, stating, “Mass deportation will

be a labor-market disruption celebrated by American workers, who will now be offered higher wages with better

benefits to fill these jobs” (“Amendment Text”). These claims oversimplify the labor market, which is dynamic and

influenced by factors like consumer demand, technological change, and global trade.

Evidence suggests that unauthorized immigrants complement, rather than replace, U.S. workers. They typically fill

low-wage, labor-intensive roles in agriculture, construction, and hospitality– jobs that U.S.-born workers are less

likely to pursue (Krogstad et al.). By supporting these industries, unauthorized workers enable job creation in

higher-skilled or supervisory roles for U.S. citizens (Shepperson). For example, studies show that immigrant labor

in agriculture supports supply chains that sustain thousands of U.S. jobs in processing and distribution

(Gutiérrez-Li). The notion of a fixed job pool ignores how immigrants contribute to economic growth, creating demand

that generates additional employment opportunities.

C. Historical Lessons from Mass Deportations

Historical precedents highlight the risks of mass deportations. During the Obama administration, the Secure

Communities initiative (2008–2014) deported approximately 400,000 unauthorized immigrants (Gonzalez-Barrera and

Krogstad). Contrary to claims that deportations benefit U.S. workers, this program reduced employment and hourly

wages for U.S.-born individuals (East et al.). Research indicates that for every 1 million unauthorized workers

deported, 88,000 U.S. native workers were driven out of employment (Clemens). These were not temporary layoffs but

persistent declines in available jobs, as businesses scaled back operations due to labor shortages (Watson). The

hardest-hit were the least educated and most vulnerable U.S. workers—ironically, a demographic that aligns with

Trump’s core supporter base. The policy “substantially harmed U.S. workers,” reducing both their employment and

wages, and failed to create net job gains (Clemens). This historical example suggests that Trump’s proposed

deportations could similarly backfire, disrupting the labor market and harming the very workers they aim to

protect.

D. Economic Consequences of Mass Deportations

Mass deportations would deliver a profound shock to the U.S. labor market. The Peterson Institute for International

Economics estimates that deporting 1.3 million workers would reduce U.S. employment by 0.6% below the baseline, with

effects persisting over time (Peterson et al.). This disruption would exacerbate existing labor shortages, with

industries like agriculture, construction, and hospitality facing immediate challenges (Joint Economic Committee).

For example, a significant reduction in farmworkers could increase grocery prices by 10–20%, according to USDA

projections, as fewer workers harvest crops (“USDA Agricultural”). In construction, labor shortages could delay

projects and raise housing costs, worsening affordability issues. The hospitality sector would face service delays

and higher prices, impacting tourism and local economies (Payan and José Iván Rodríguez-Sánchez).

Furthermore, these shortages would have ripple effects across the economy. Reduced production would push up

consumer prices for goods and services, from groceries to childcare, fueling inflation (DePillis). The Congressional

Budget Office estimates that immigration, including unauthorized immigration, boosts GDP by 1–2% annually (“Effects

of the Immigration Surge”). Mass deportations could reverse these gains, with Brookings projecting a 0.5% GDP drop

in 2025 alone (Esterline et al.). Reduced consumer spending due to higher prices could further weaken retail and

other sectors, amplifying economic disruption.

E. Fiscal Impacts

Unauthorized immigrants contribute significantly to public finances, despite being ineligible for most federal

benefits (Costa et al.). Through sales, property (via rent), and payroll taxes, they “contributed $30.8 billion in

total taxes” in 2021, per the American Immigration Council (Hubbard). The Congressional Budget Office projects that

immigration will reduce federal deficits by $900 billion over the next decade (“Effects of the Immigration Surge”).

However, Trump’s deportation plan would shrink this tax base while incurring substantial enforcement costs. The

American Immigration Council estimates that deporting approximately 13.3 million immigrants could cost at least $315

billion, covering arrests, detention, legal processing, and removals (“Mass Deportation”). This would increase

federal deficits, as the loss of tax revenue and high enforcement costs outweigh any savings from reduced public

service use.

F. Conclusion

President Trump’s 2025 mass deportation agenda, while aimed at protecting American workers, risks significant

economic disruption. Historical evidence from the Secure Communities initiative shows that deportations can harm

U.S. workers, particularly the most vulnerable, by reducing employment and wages (Ambrosius and Velásquez).

Unauthorized immigrants, far from “taking jobs,” fill critical labor gaps in agriculture, construction, and

hospitality, supporting economic growth and keeping consumer prices low (“Unauthorized Immigrant Population”). Their

removal would trigger labor shortages, inflate prices, and strain public finances, potentially costing $315 billion

while reducing GDP and tax revenue (“Mass Deportation”). As the U.S. navigates this policy, policymakers must weigh

these economic realities against political rhetoric. Alternatives, such as comprehensive immigration reform or

targeted enforcement, could better balance economic stability and national priorities, ensuring that America’s

workforce and economy remain resilient (Beaudouin).

Works Cited

AFP. “Trump’s Mass Deportation Plan Could End up Hurting Economic Growth.” Dawn, 25 Nov. 2024,

www.dawn.com/news/1874599/trumps-mass-deportation-plan-could-end-up-hurting-economic-growth. Accessed 18 June

2025.

Ambrosius, Christian, and Andrea Velásquez. “Large-Scale Deportations May Have Unintended Consequences.”

Migrationpolicy.org, 2 Oct. 2024, www.migrationpolicy.org/article/deportations-unintended-consequences. Accessed

18 June 2025.

“Amendment Text: H.Amdt.811 to H.R.5283 - 118th Congress (2023-2024).” Congress.gov, 2023,

www.congress.gov/amendment/118th-congress/house-amendment/811/text. Accessed 8 June 2025.

Beaudouin, Will. “A New Immigration System to Safeguard America’s Security, Expand Economic Growth, and Make Us

Stronger.” Center for American Progress, 6 July 2025,

www.americanprogress.org/article/a-new-immigration-system-to-safeguard-americas-security-expand-economic-growth-and-make-us-stronger/.

Accessed 12 June 2025.

Bender, Michael C. “On the Trail, Trump and Vance Sharpen a Nativist, Anti-Immigrant Tone.” Nytimes.com, The New

York Times, 22 June 2024, www.nytimes.com/2024/09/22/us/politics/trump-vance-nativist.html. Accessed 9 June

2025.

“Can America’s Economy Cope with Mass Deportations?” The Economist, 6 Jan. 2025,

www.economist.com/finance-and-economics/2025/01/06/can-americas-economy-cope-with-mass-deportations. Accessed 12

June 2025.

Clemens, Michael A. “Trump’s Proposed Mass Deportations Would Backfire on US Workers.” PIIE, 6 Mar. 2024,

www.piie.com/blogs/realtime-economics/2024/trumps-proposed-mass-deportations-would-backfire-us-workers. Accessed 5

June 2025.

Costa, Daniel, et al. “Unauthorized Immigrants and the Economy.” Economic Policy Institute, 15 Apr. 2025,

www.epi.org/publication/unauthorized-immigrants/. Accessed 8 June 2025.

DePillis, Lydia. “How Trump’s Immigration Plans Could Affect the Economy.” The New York Times, 13 Nov. 2024,

www.nytimes.com/2024/11/13/business/economy/trump-immigration-inflation-prices.html. Accessed 9 June 2025.

East, Chloe N, et al. “The Labor Market Effects of Immigration Enforcement.” Journal of Labor Economics, vol. 41,

no. 4, 6 June 2022, https://doi.org/10.1086/721152.

“Effects of the Immigration Surge on the Federal Budget and the Economy | Congressional Budget Office.”

www.cbo.gov, Congressional Budget Office, 23 July 2024, www.cbo.gov/publication/60165. Accessed 8 Aug. 2025.

Esterline, Cecilia, et al. “Immigration and the Macroeconomy after 2024.” Brookings, 16 Oct. 2024,

www.brookings.edu/articles/immigration-and-the-macroeconomy-after-2024/. Accessed 8 June 2025.

Gonzalez-Barrera, Ana, and Jens Manuel Krogstad. “U.S. Deportations of Immigrants Reach Record High in 2013.” Pew

Research Center, 2 Oct. 2014,

www.pewresearch.org/short-reads/2014/10/02/u-s-deportations-of-immigrants-reach-record-high-in-2013/. Accessed 8

June 2025.

Gutiérrez-Li, Alejandro. “Feeding America: How Immigrants Sustain US Agriculture.” Baker Institute, 19 July 2024,

www.bakerinstitute.org/research/feeding-america-how-immigrants-sustain-us-agriculture. Accessed 18 Sept. 2025.

Hubbard, Steven. “Dispelling the Myth: How Undocumented Immigrants Pay Taxes and Contribute to the US Tax Base -

American Immigration Council.” American Immigration Council, 22 Mar. 2023,

www.americanimmigrationcouncil.org/blog/how-undocumented-immigrants-pay-taxes-itin/. Accessed 5 June 2025.

Joint Economic Committee. “Mass Deportations Would Deliver a Catastrophic Blow to the U.S. Economy - Mass

Deportations Would Deliver a Catastrophic Blow to the U.S. Economy - United States Joint Economic Committee.”

Senate.gov, 11 Dec. 2024,

www.jec.senate.gov/public/index.cfm/democrats/2024/12/mass-deportations-would-deliver-a-catastrophic-blow-to-the-u-s-economy.

Accessed 12 June 2025.

Krogstad, Jens Manuel, et al. “A Majority of Americans Say Immigrants Mostly Fill Jobs U.S. Citizens Do Not

Want.” Pew Research Center, 10 June 2020,

www.pewresearch.org/short-reads/2020/06/10/a-majority-of-americans-say-immigrants-mostly-fill-jobs-u-s-citizens-do-not-want/.

Accessed 10 June 2025.

“Mass Deportation - American Immigration Council.” American Immigration Council, 6 June 2025,

www.americanimmigrationcouncil.org/report/mass-deportation/. Accessed 8 Apr. 2025.

Payan, Tony, and José Iván Rodríguez-Sánchez. “Social and Economic Effects of Expanded Deportation Measures.”

Issue Brief, 26 Mar. 2025,

www.bakerinstitute.org/research/social-and-economic-effects-expanded-deportation-measures. Accessed 5 June

2025.

Peterson, et al. “Replication Dataset and Calculations for PIIE WP 24-20 the International Economic Implications

of a Second Trump Presidency by Warwick McKibbin, Megan Hogan, and Marcus Noland (2024).” PIIE, 26 Sept. 2024,

www.piie.com/publications/working-papers/2024/international-economic-implications-second-trump-presidency.

Accessed 13 June 2025.

Shepperson, Anna. “Immigrants Are Key to Filling US Labor Shortages, New Data Finds - American Immigration

Council.” American Immigration Council, 2 July 2024,

www.americanimmigrationcouncil.org/blog/immigrants-fill-us-labor-shortages-map-the-impact/. Accessed 13 June

2025.

The Economic and Fiscal Impacts of Mass Deportation: WHAT’S at RISK in WASHINGTON STATE. Washington State Budget

and Policy Center.

The Economist. “The Economics of Mass Deportations.” YouTube, 3 Feb. 2025, www.youtube.com/watch?v=sXPMxHmOaPc.

Accessed 3 June 2025.

“Unauthorized Immigrant Population Trends for States, Birth Countries and Regions.” Pew Research Center, 12 June

2019, www.pewresearch.org/race-and-ethnicity/feature/unauthorized-trends/. Accessed 4 June 2025.

“Unauthorized Immigrants Today - American Immigration Council.” American Immigration Council, Oct. 2014,

share.google/DieQrjnUTw4fROgGZ. Accessed 8 June 2025.

Watson, Tara. “Immigrant Deportations: Trends and Impacts | Econofact.” Econofact | Key Facts and Incisive

Analysis to the National Debate on Economic and Social Policies., 9 Oct. 2024,

econofact.org/immigrant-deportations-trends-and-impacts. Accessed 8 June 2025.

How have Trump’s tariffs affected the international supply chain?

Katelyn To

In a world where the supply chain never gets to recover, President Donald J. Trump’s tariff trade war is

jeopardizing an economy that seemed like it was finally returning to normalcy. From launching a trade war the second

he’s back in the office to leading an average tax hike of $1,243 per US household in 2025, Trump’s tariffs have

forced the global supply chain to experience immense distress causing a ripple effect. These tariffs have disrupted

inventory planning and precision of demand forecasting within the supply chain which will “lead companies to pause

or cancel orders and beg or plead with vendors,” according to Brain Wench, CEO of Flat World Global Solutions. Due

to the increased uncertainty, many companies are reducing their purchasing activities with transportation rates

decreasing, logistics firms facing challenges and more.

An example of a threatened supply chain is the automotive industry, one of the most heavily impacted chains since

the tariffs. On what Trump called “Liberation Day”, he announced 25% tariffs on all vehicle imports to the US with

certain exemptions. Following the announcements, stock prices of huge OEMs have significantly decreased including

Ford, GM, Stellantis, Tesla, Rivian and Toyota Motor North America. Shortly after, OEMSs started taking immediate

action starting with JLR pausing all vehicles, Stellantis temporarily laying off 900 US workers and VW group

suspending vehicle shipments from Mexico and Canada, with its Audi division suspending exports to the US from Europe

and Mexico.

The ongoing trade war between the US and China has added another level of uncertainty to the automotive industry,

particularly EVs. Earlier this week, Trump hiked tariffs to 104%, and China responded with tariffs on US imports to

up to 84%. Currently, China faces 145% tariffs on all imported goods and China responds with tariffs of 125% on US

goods. This has impacted Tesla with customer data showing that the US shipped close to $3.1 billion worth of

vehicles to China last year leading to Tesla having to halt new orders in China on US imported models. However,

Europe may potentially be affected by this as its EV supply chain is closely linked and reliant on Chinese

imports.

The good news is that the global supply chain is still arguably one of its most resilient stages in memory. Due to

the pandemic and the geopolitical tensions since 2022, companies have become more flexible and innovative in their

approach. According to Wench, businesses have been navigating these challenges by leveraging technology and data to

make decisions.

“The pandemic taught us we need to allow flexibility in our supply chains, maybe at the cost of pennies,” says

Wench.

Ultimately, while tariffs pose significant changes, there are more optimistic predictions that depend on the

assumption that the current period of instability is temporary. If the disruption is indeed short term, similar to

the period during the first Trump administration, the supply chain may have already endured the worst part. If the

disruptions continue as an effort to isolate the US from the global economy, this period may be considered

straightforward in hindsight.

Works Cited

Engelland, Bryce. “The Global Supply Chain’s Reaction to the Trump Tariffs: Crash, Maneuver & Stand-by - Thomson

Reuters Institute.” Thomson Reuters Institute, 14 Apr. 2025,

www.thomsonreuters.com/en-us/posts/corporates/supply-chains-reaction-tariffs/. Accessed 25 Apr. 2025.

jameslopresti. “How Trump’s Tariffs Are Impacting the Global Supply Chain.” Online Degrees - Florida Institute of

Technology | Florida Tech Online, May 2023,

www.floridatechonline.com/blog/process-improvement/how-trumps-tariffs-are-impacting-the-global-supply-chain/.

Accessed 25 Apr. 2025.

“Tracking the Economic Impact of the Trump Tariffs.” Tax Foundation, 18 Apr. 2025,

taxfoundation.org/research/all/federal/trump-tariffs-trade-war/?utm_source=chatgpt.com. Accessed 25 Apr. 2025.

Hall, Kalea, et al. “Stellantis to Temporarily Lay off 900 US Workers as Tariffs Bite.” Reuters, 3 Apr. 2025,

www.reuters.com/business/autos-transportation/stellantis-says-will-temporarily-lay-off-900-us-workers-following-tariff-2025-04-03/.

Accessed 25 Apr. 2025.

Reuters. “Trump to Exempt Carmakers from Some US Tariffs, FT Says.” Reuters, 23 Apr. 2025,

www.reuters.com/business/autos-transportation/trump-exempt-carmakers-some-us-tariffs-ft-says-2025-04-23/?utm_source=chatgpt.com.

Accessed 25 Apr. 2025.

Articles: (Head of Articles) Konnor Wan; Tim He, Howard Deng, Colin Ngan, Sebastian Zhu, Thomas

Wu, Chloe Luo, Samson Suen, Natalie Yue, Monique Siu, Eason Huang, Helen Dai, Athena Yip, Isabella Sun, Kaleb Lau,

Judy Bai, Amy Liu, Joseph Wu, Bruce Chan, Tony Huang, Richard Zeng, Sebastian Ng, Sofie Tse, Claire Fang, Katelyn

To;

Layout: (Head of Layout) Justin Chen;

Marketing: (Head of Marketing) Sophia Swing; Daisy Chen, Irene Chen, Zoe Wai, Athena Yip, Arthur

Wong, Katelyn To, Jocelyn Tam, Micky Lyu;

Administration: Tim He, Howard Deng, Colin Ngan, Sebastian Zhu, Konnor Wan, Elly Gao;

Interview: Helen Dai, Arthur Wong, Katelyn To, Howard Deng, Colin Ngan;

Filming: Athena Yip, Jocelyn Tam, Sophia Swing, Sebastian Zhu, Tim He;